How to Calculate Inventory Turnover

The inventory turnover ratio is an important efficiency metric and compares the amount of product a company has on hand, called inventory, to the amount it sells. In other words, inventory turnover measures how many times inventory has sold during a period.

Key Takeaways

- Inventory turnover is a ratio that shows how many times inventory has sold during a specific period of time.

- Dividing the cost of goods sold (COGS) by the average inventory during a particular period will give you the inventory turnover ratio.

- The ratio helps the company understand if inventory is too high or low and what that says about sales relative to inventory purchased.

Calculating Inventory Turnover

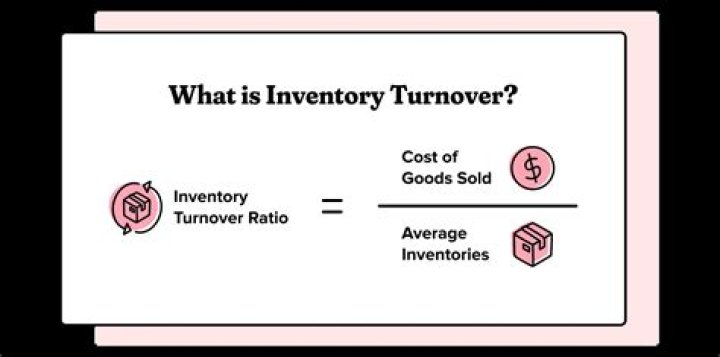

The inventory turnover ratio can be calculated by dividing the cost of goods sold by the average inventory for a particular period.

The reason average inventory is used is that most businesses experience fluctuating sales throughout the year, so the use of current inventory in the calculation can produce skewed results. For example, inventory for retailers like Macys Inc. (M) might rise during the months leading up to the holidays and fall during the months following the holidays.

Average inventory is typically used to calculate inventory turnover to account for seasonal variations in sales. The average inventory is calculated by adding the inventory at the beginning of the period to the inventory at the end of the period and dividing by two.

Average inventory is used in the ratio so as to account for the normal seasonal ebb and flow of sales.

Inventory Turnover Ratio Formula

Inventory Turnover = Cost Of Goods Sold / ((Beginning Inventory + Ending Inventory) / 2)

The calculation of inventory turnover can also be done by dividing total sales by inventory. However, because sales are typically recorded at market value and inventory recorded at cost, this comparison can produce falsely inflated results.

Most companies use the cost of goods sold (COGS) for the numerator instead of total sales because COGS reflects the total cost of producing goods for sale and excludes retail markup.

Interpreting Inventory Turnover

Companies use the inventory turnover ratio to help inform decisions about production, sales performance, and marketing.

The ratio provides management with insight into inventory purchasing and sales performance. If for example, inventory is high, it might be an indication that either the company’s sales are underperforming or too much inventory was purchased. In response, either sales need to increase, or the excess inventory may cost the company in storage fees.

It’s important that sales and inventory purchases are in line with each other. If the two are not in sync, it will ultimately show up in the inventory turnover ratio.

Example of Inventory Turnover

A company has the following figures on their books:

- Cost of goods sold totaling $150,000

- Beginning inventory of $75,000

- Ending inventory of $12,000, reflecting the effect of seasonal sales

The inventory turnover rate for this period is calculated by:

- $150,000 / (($75,000 + $12,000) / 2)

- Inventory turnover ratio = 3.45

This indicates that the company has sold its entire average inventory more than three times during the given period.

Why Inventory Turnover Matters

The optimal inventory turnover ratio depends on the business and the industry in question, so a company’s current inventory ratio should always be compared to its past performance, as well as to the performance of other companies within its industry.

A low ratio could be an indication either of poor sales or overstocked inventory. Poor sales can be the result of ineffective advertising, poor quality, inflated price or product obsolescence. Excess inventory can also be costly since inventory sitting in a warehouse costs the business money to produce but generates no revenue.

While a high inventory turnover ratio is preferable to a low ratio, it’s not always an indication of an efficient business model. A high ratio could reflect robust sales. However, a high ratio could also be because of low inventory levels, and if orders can’t be filled on time to match sales, the company could lose customers.

Inventory turnover reflects a company’s liquidity. For example, if inventory cannot be turned quickly, a company might run into cash flow problems. However, a company with a higher more efficient turnover rate would be able to generate cash very quickly.

Banks and creditors typically use inventory as collateral for loans. As a result, it’s important for a company to demonstrate they have the sales to match their inventory purchases and that the process is managed properly.

Inventory turnover ratios vary by industry. For example, car companies might have a lower ratio than clothing companies.

All the information necessary to calculate a business’s inventory turnover is available on its financial statements. COGS can be found on the income statement, and both beginning and ending inventory can be found on the balance sheet.

Inventory turnover is a critical accounting tool that retailers can use to ensure they are managing the store’s inventory well. In its most basic definition, it is how many times during a certain calendar period that you sell and replace (turnover) your inventory.

The figure you end up with will indicate how fast the products sell on average. Inventory turnover can help you gauge how sales strategies are affecting the retail store’s bottom line over time. Turnover is also an indicator of the quality of your customer experience. You will see that as I explain more.

What Is the Significance of Inventory Turnover?

Retailers that handle inventory need to know how quickly their products sell and how often they need to replace them. Manufacturers and wholesalers keep track of their ‘turns’ and retailers should do the same. Manufacturers don’t want to be stuck with a lot of leftover inventory at the end of the season. The markdowns they take are just like the ones you do if you have leftover inventory.

Inventory turnover will help you understand – in concrete numbers – how your current inventory strategy is working. Are you stocking too much? Are you stocking too little? Are you stocking products that customers don’t want? Are you seeing great results from a recent change in product or marketing?

Also called “stock turns” or “stock turnover,” inventory turnover is a vital number to your retail business’s accounting. When it is used with the rest of the data on your profit & loss sheets, it can give you useful insights into the health of your business. It can also help guide you to make changes if needed.

It is a good idea to calculate your turns on a regular basis. Whether you run the numbers annually, seasonally, quarterly, or monthly will depend on the size, type, and age of your store.

How to Calculate Inventory Turnover

Controlling inventory turnover is key to keeping your shelves stocked with interesting, fresh products that keep the cash flowing – after all cash is king in retail. You want to buy the merchandise, move it quickly, and then repurchase more products for your customers.

In general, higher inventory turns are a good indicator that you’re moving merchandise, which should mean that business is good. However, if the turnover becomes too high, sales may be lost because of reduced customer selection.

Inventory turnover can be calculated in whole, as well as by department or merchandise category. In fact, you should always look at your turnover metrics by department. Some items just turn slower than others.

In order to calculate inventory turnover, you need to know two numbers: Cost of goods sold (COGS) and average inventory.

To find your COGS:

COGS = Beginning Inventory + Purchases – Ending Inventory

This should include your wholesale costs for the inventory and any additional costs, such as shipping and handling, that you have paid. Also, be sure to subtract the cost of any scrapped or lost items.

To find your average inventory:

Average Inventory = Beginning Inventory + Ending Inventory / 2

The values of your inventory should be found on the company balance sheet for each accounting period.

To calculate your inventory turnover:

Inventory Turnover = COGS / Average Inventories

The result you come up with will give you the inventory turnover ratio. If you divide that into the number of days used in your accounting period, you receive the average number of days that you held the inventory.

Days Inventory Held = Days in Accounting Period / Inventory Turnover Ratio

An Example of Calculating Inventory Turnover

Let’s use a set of easy, fictional sales numbers to put these calculations into perspective.

- Opening inventory: $10,000

- Closing inventory: $20,000

- Additional purchases: $50,000

- Number of days in period: 90

| Cost of Goods Sold | $10,000 + $50,000 – $20,000 | = $40,000 |

| Average Inventory | $10,000 + $20,000 / 2 | = $15,000 |

| Inventory Turnover Ratio | $40,000 / $15,000 | = 2.67 |

| Average Days Held in Inventory | 90 / 2.67 | = 33.7 |

With this example, the retailer held onto their inventory an average of 33 days in a 90-day period. They are turning over about once a month. Is this a good turnover rate? All that depends on your merchandise.

One of the best practices for retailers is to join a trade association where they can compare numbers and results with similar retailers. In other words, compare your turns with another shoe store (since you sell shoes too) versus a sporting goods store.

How to Calculate the Inventory Turnover Ratio

- Share

- Pin

The inventory turnover ratio is a formula that makes it easy to figure out how long it takes for a business to sell through its entire inventory. A higher inventory turnover ratio usually indicates that a business has strong sales compared to a company with a lower inventory turnover ratio.

Learn how to calculate this ratio and how to use it to analyze companies.

What Is the Inventory Turnover Ratio?

The inventory turnover ratio is a straightforward method for determining how often a company turns over its inventory in a specified period of time. It’s also known as “inventory turns.” This formula provides insight into the efficiency of a company when converting its cash into sales and profits.

The inventory turnover ratio is an example of an efficiency ratio.

How Do You Calculate the Inventory Turnover Ratio?

The first step in calculating the inventory turnover ratio is to choose a timeframe to measure (eg, a quarter or a fiscal year). Then, find the average inventory for that period by averaging the ending and beginning costs of inventory for the timeframe in question. Once you have your timeframe and average inventory, simply divide the cost of goods sold (COGS) by the average inventory.

How the Inventory Turnover Ratio Works

You can save yourself a lot of trouble when assessing inventory turnover ratios by acquiring a company’s balance sheet and income statement. COGS is usually listed on the income statement, and inventory balances will be found on the balance sheet. With these two documents, you just need to plug the numbers into the simple ratio formula, and you’re done.

If you compare figures with other analysts, it’s important to note that some analysts use total annual sales instead of the cost of goods sold. This is largely the same equation, but it includes a company’s markup, so it can lead to a different result than equations that use the cost of goods sold. One isn’t necessarily better than the other, but it is important to be consistent with your comparisons. Using annual sales to calculate the ratio for one company while using the cost of goods sold for another company won’t give you any real sense of how the two companies compare.

An Example

Consider this real-world example. Coca-Cola’s income statement from 2017 showed that the COGS was $13.256 million, and its average inventory value between 2016 and 2017 was $2.665 million. We can use these figures to calculate the ratio:

- Inventory turns = COGS / average inventory

- Inventory turns = $13.256 million / $2.665 million

- Inventory turns = 4.974

Now you know that Coca-Cola’s inventory turns for that year was 4.974. You can compare this ratio to others in the soft drink and snack food industry to understand how well Coca-Cola is doing. If, for example, you found out that a competitor’s inventory turns was 8.4, that would signal that the competitor is selling product more quickly than Coca-Cola.

There are many reasons why a company may have fewer inventory turns than another company—it doesn’t necessarily mean that one company is worse than the other. It’s important to read a company’s financial statements and any accompanying disclosure notes to get a full picture. Although Coca-Cola’s inventory turn rate was lower, you might find other metrics that show that it was still financially stronger than the other averages for its industry. Using historical data to compare current years to previous years could also provide helpful context.

Generally speaking, the more a company’s assets are tied up in inventory, the more reliant that company is on faster turnover.

Inventory Turnover Days

You can take inventory analysis a step further by using the inventory turn rate to calculate the number of days it takes for a business to clear its inventory.

Continue with the Coca-Cola example, which provided an inventory turnover ratio of 4.974. Divide 365 by that inventory turns number, which should give you a result of 73.38. That means, on average, it took Coca-Cola 73.38 days to sell its inventory. This puts the company’s efficiency in another context. Calculating the inventory turnover days doesn’t necessarily provide any new information, but framing the same information in terms of days is helpful for some analysts.

Limitations of the Inventory Turnover Ratio

The time it takes a company to sell its inventory can vary greatly by industry, so if you don’t know the average inventory turns for the industry in question, then the formula won’t help your analysis all that much.

For example, retail stores and grocery chains typically have a much higher inventory turn rate because they sell lower-cost products that spoil quickly. As a result, these businesses require far greater managerial diligence. On the other hand, companies that manufacture heavy machinery, such as airplanes, will have a much lower turnover rate. It takes a long time to manufacture and sell an airplane, but once the sale closes it often brings in millions of dollars for the company.

How to Calculate the Weeks of Inventory on Hand

Inventory turnover can refer to anything from how long a box of cereal sits on a grocery store shelf to the frequency with which a mutual fund manager buys and sells securities. Calculating inventory turnover ratio is relatively simple and the necessary information is readily available. Knowing the rate of inventory turnover gives you insight into a business’s management efficiency or investment fund’s philosophy.

Inventory Turnover Defined

Inventory turnover ratio, also called inventory turns, measures the cost of goods sold as a proportion of the value of a firm’s average inventory. Put another way, this ratio tells you how many times each year a business uses up and replaces its inventory. The yearly cost of goods sold is stated near the top of a company’s income statement, which you’ll find in its annual report. The value of inventory is located in the assets section of a company’s balance sheet, also published in the annual report.

Figuring the Turnover Rate

To compute an inventory turnover ratio, divide the cost of goods sold by the average inventory value. Calculate average inventory value by adding the inventory values from the current year and previous year balance sheets, and divide the sum in half.

Suppose a business reports its year’s cost of goods sold on the income statement as $1.5 million and you determine the average inventory equals $600,000. Dividing $1.5 million by $600,000 gives you an inventory turnover ratio of 2.5 times per year.

High and Low Inventory Turnover

Analysts compare inventory turnover ratios of similar companies because typical ratios vary from industry to industry. For instance, grocery stores with perishable stock normally have higher turnover ratios than dealers in durable goods such as home appliances. The important thing is that inventory turnover ratio indicates how well a firm manages its inventory. A low ratio may indicate excess inventory that can raise storage costs and increase the risk of outdated merchandise. However, excessively high ratios suggest the business may be prone to inventory shortfalls that can result in lost sales and unhappy customers.

Investment Fund Inventory Turnover

Inventory turnover ratio for an investment fund means something different than the turnover ratio of a business’s physical merchandise. For a fund, calculate inventory turnover by first subtracting short-term assets that mature in less than 12 months. Pick the lesser of the fund’s securities acquisitions or assets sold and divide by the average net value of the fund’s portfolio. According to Accounting Explained, low ratios of around 20 to 30 percent of net assets indicate the fund manager follows a “buy and hold” investment philosophy. Funds with ratios greater than 100 percent are likely to be run according to an aggressive investment strategy.

Join the Community

Inventory turnover refers to the amount of times inventory is sold and replaced within a given period, such as a year. Low turnover rates can suggest that stores are acquiring a surplus of inventory, which can mean that they are experiencing problems, while a high turnover rate indicates that a store is doing brisk business. Inventory turnover is one of the many metrics used to gauge the financial health of companies large and small, and business owners may periodically assess their inventory turnover to see how they are doing.

Inventory turnover refers to the amount of times inventory is sold and replaced within a given period, such as a year.

Two different formulas can be used to arrive at inventory turnover numbers. In the first, people divide the cost of sales by the inventory. However, this method can be flawed because inventories are usually expressed in wholesale value, not in retail value, which means that the result of this equation will be skewed. Instead, some people prefer to divide the cost of goods sold, reflecting the price paid by the company, by the average inventory. Using an average inventory avoids skewed results caused by seasonal changes, such as radical differences in inventory which appear in November and December in many regions of the world.

Sometimes, the rate is low because a company is stocking up on goods in preparation for a big event, in which case the company may be perfectly healthy despite the fact that it has a low inventory turnover ratio. Conversely, extremely high rates can serve as an alert that a store may not be keeping adequate supplies in stock, and the consumers could be growing frustrated with a lack of options caused by poor inventory management. Companies must seek a balance when managing their inventory, using their funds wisely to generate the best returns.

Barcode scanners and other asset tracking technology can be used to monitor inventory and analyze sales patterns.

People managing their inventories must also think about how they are going to allocate funds. For example, a company could buy a very large batch of a particular item, tying up capital in inventory until it sells, or it could buy a small batch, use the funds from that sale to buy another small batch, and so forth, thereby freeing up funds for other uses. Keeping too much costly inventory on hand can be a bad idea for a company which needs financial flexibility, as it may be forced to sell off the inventory quickly to raise capital.

Performing routine inventory checks can help a company track turnover rates.

Inventory turnover also reflects consumer interest in the products a company is selling. If a company experiences a high turnover rate which gradually slides into a low one, it suggests that consumer interest may be cooling, and that it is time to make some adjustments to the inventory. Conversely, if a company’s turnover rate suddenly starts to skyrocket, it means that there has been a spike in consumer interest which should be addressed.

Low inventory turnover rates may indicate that a store is acquiring a surplus of inventory.

Ever since she began contributing to the site several years ago, Mary has embraced the exciting challenge of being a wiseGEEK researcher and writer. Mary has a liberal arts degree from Goddard College and spends her free time reading, cooking, and exploring the great outdoors.

How To Calculate Inventory Turns

Inventory Turns is the number of times your inventory turns (is used or replaced with new product) during a given period (month, year, whatever you choose). Typically, the higher the turns the better because it indicates that product is purchased and used on an “as needed” basis and is not just sitting on the shelves. Typical industry standards for Inventory Turns in restaurants is 4 – 8 turns a month. The higher the ratio of fresh product to frozen/dry product you use the higher the number should be.

Inventory Turn Formula

The formula to calculate inventory turns is:

inventory used ÷ average inventory

First, calculate average inventory for the period. If you take a monthly inventory, this is the formula to calculate average inventory for the month:

beginning inventory + ending inventory ÷ 2

Next, calculate inventory used:

= beginning inventory + purchases – ending inventory

Lastly, calculate inventory turns:

inventory used ÷ average inventory

| Calculate Inventory Turns Example | ||

| Beginning Inventory | $3,490 | |

| Purchases | $22,873 | |

| Sub-Total | $26,363 | BI+P |

| Ending Inventory | $6,129 | |

| Inventory Used | $20,234 | ST-EI |

| Average Inventory | $4,809 | (BI + EI) ÷ 2 |

| Inventory Turns | 4.21 | IU ÷ AI |

Average Inventory = $4809.50 ($3490 + $6129) ÷ 2

Inventory Turns = 4.21 ($20,234 + $4809.50)

Inventory Change = + $2639 or + 176%

Comments from before Site Migration

CALLIE [174.115.116.186] [ May 08, 2015 ]

Your Website is a Wonderful Teaching Tool! I learned a lot about the complexities of running a restaurant and appreciate the work invested in this. Thanks so much for sharing.

Thanks Kiran! Pretty cool that you have set the site as your homepage!!

may i say this is an amazing website. I have made it my homepage, and make it a point to read at least an article everyday. Thank you so very much for all the hard work you have put in , so newcomers like me can gain from the knowledge you have acquired.

Jeremy – Awesome! It’s nice to know people find the info here useful. Next time you come into Blackfish say “hi”. I’m usually there everyday except mon/tue.

I agree with Mike. I have been turning to this site for years now to learn and apply to my establishment. As a Chef it is hard to find the time to do all of these worksheets myself. This site has been invaluable to me! Also, I would like to add that I love eating at the Blackfish. I have had everything on the menu and it is all fantastic.

Nice work and thank you very much.

Michael – Thanks so much for the feedback! It is a lot of work…so hearing that folks are returning on a regular basis is very gratifying.

This site has been relevant and useful for years now. I know this isn’t the exact place to put this, but thank you for all the hard work you put into this site. Its been a go to for me for a while.

Inventory turnover represents the number of times a company sells its inventory and replaces it with the new stock over the course of a certain time period, such as a quarter or year. The ratio result can tell you how effectively the company sells and how well it manages its costs.

Defining ‘Inventory’

A company’s inventory consists of all the goods it offers for sale. For example, a company may buy wholesale items, such as clothing or gift items, and resell them. Its entire inventory is made up of finished goods.

Manufacturing companies have an inventory made up of raw goods, or various product components, works in progress, and finished items. For example, the leather pieces used to make boots would be inventory for a boot maker. All of these units qualify as inventory and are recorded in inventory and work-in-progress accounts that show up as assets on the company’s balance sheet.

The Inventory Turnover Ratio

The inventory turnover ratio is an important financial ratio for many companies. Of all the asset-management ratios, it gives the business owner some of the most important financial information, by showing how many times the company turns its inventory over within the given period.

The inventory turnover ratio measures the efficiency of the business in managing and selling its inventory in a timely manner. This ratio gauges the liquidity of the firm’s inventory and also helps the business owners determine how they can increase sales through inventory control.

Use either of the following formulas for the inventory turnover ratio:

Net Sales / Average Inventory = # of times turned over

Cost of Goods Sold / Average Inventory = # of times turned over

In order to calculate the ratio, use the figure for net sales or cost of goods sold from the company’s income statement and inventory from its balance sheet. Cost of goods sold includes the cost of raw materials, plus the cost of any direct labor or direct factory overhead to produce the inventory goods for sale.

Many analysts use an average inventory number to account for seasonality. For example, some companies may sell more during the last three months of the year because of the holiday season, so they would average inventory using balances at different points of the year rather than just using year-end inventory.

Interpreting the Result

High turnover ratio. Generally, companies want a high inventory ratio because it indicates that the company is efficiently managing and selling their inventory. The faster the inventory sells, the smaller the amount of funds the company has tied up in inventory, and the higher sales level and corresponding profits it achieves.

Companies with a high inventory turnover must be very diligent about reordering to prevent stockouts. If the company’s turnover ratio is too high, it means it sells out too fast and might be missing out on sales because it can’t keep items in stock. This could reveal an opportunity for a price increase due to high demand.

Low ratio result. A company with a low inventory turnover ratio may be holding obsolete or slow-moving inventory that is difficult to sell or has low demand. This ties up the company’s capital and eats into its profit, especially if the company relies too much on discounting in attempts to stimulate sales.

However, the company may also be holding a lot of inventory for legitimate reasons. A retailer could be preparing for a holiday season; on the other hand, perhaps its suppliers are planning a strike or long holiday—such as for Chinese New Year when Chinese factories completely shut for almost a full month.

The Ratio and Efficiency

An efficiently run company would want to synchronize its sales and inventory levels as much as possible. Too little inventory means lost sales, while too much inventory means tied-up capital for inventory that’s not selling fast enough.

If the company’s cost of goods is out of line with inventory turnover, it might be spending too much to produce units of inventory that don’t sell quickly enough.

The inventory turnover ratio—especially when compared to historical periods, or to the same ratio from the company’s peers or competition—can tell a lot about the effectiveness of the company’s sales and purchasing teams.

Ultimately, business owners should understand why their company’s inventory turnover ratio is high or low and take action where needed. Looking at the company’s investment in inventory and determining, by product or product group, which inventory is turning over the quickest with the highest profit can help identify the products to keep stocking and those to discontinue.

The inventory turnover ratio is used in fundamental analysis to determine the amount of times a company sells and replaces its inventory over a fiscal period. The inventory turnover ratio compares a company’s sales and its inventory. To calculate a company’s inventory turnover, divide its sales by its inventory. Similarly, the ratio can be calculated by dividing the company’s cost of goods sold (COGS) by its average inventory.

Explaining How to Calculate the Inventory Turnover Ratio in Excel

Compare the inventory turnover ratios between Ford Motor Company and General Motors Company using Microsoft Excel. For the fiscal period ending Dec. 31, 2014, Ford Motor Company had inventory of $7.866 billion and total revenue, or total sales, of $144.077 billion. General Motors Company had inventory of $13.642 billion and total sales of $155.929 billion for that same fiscal period.

In Excel, right-click on columns A, B and C, and click on Column Width. Next, change the value to 30 for each of the columns. Then, click OK. Enter Ford Motor Company into cell B1 and General Motors Company into cell C1. Enter Dec. 31, 2014 into cells B2 and C2.

Next, enter Inventory into cell A3, Total Sales into cell A4 and Inventory Turnover Ratio into cell A5. Enter =7866000000 into cell B3 and =144077000000 into cell B4. Ford’s inventory turnover ratio is calculated by entering the formula =B4/B3 into cell B5. The resulting inventory turnover ratio of Ford Motor Company is 18.32.

Next, enter =13642000000 into cell C3 and =155929000000 into cell C4. Similarly, the inventory turnover ratio of General Motors Company is calculated by entering the formula =C4/C3 into cell C5. The resulting inventory turnover ratio is 11.43.

Ford’s higher inventory turnover ratio may indicate it has strong sales or there is less buying of the cars produced by General Motors Company.

Last Updated: October 18, 2019 References Approved

This article was co-authored by Michael R. Lewis. Michael R. Lewis is a retired corporate executive, entrepreneur, and investment advisor in Texas. He has over 40 years of experience in business and finance, including as a Vice President for Blue Cross Blue Shield of Texas. He has a BBA in Industrial Management from the University of Texas at Austin.

There are 12 references cited in this article, which can be found at the bottom of the page.

wikiHow marks an article as reader-approved once it receives enough positive feedback. This article received 12 testimonials and 94% of readers who voted found it helpful, earning it our reader-approved status.

This article has been viewed 646,050 times.

Managing inventory is very important in a company that sells products to make a profit. Calculating inventory days is an indicator of how well the business is doing in terms of inventory. With this information, you can compare your business’s inventory days with that of your competitors. A lower inventory days measurement means that you are achieving higher inventory turnover and a better return on assets. Calculating inventory days involves determining the cost of goods sold and average inventory in a given period. To calculate the days in inventory, you first must calculate the inventory turnover ratio, which comprises the cost of goods sold and the average inventory. Then, you’ll need to divide the number of days in the period by this inventory turnover ratio to determine days in inventory.

March 18, 2020 • Armando Roggio

How quickly a business sells its inventory is typically a strong indicator of efficiency, cash flow, and general well-being.

Imagine two online retailers selling products for home gardeners. Both companies hold about $1 million in inventory on average. But one company turns its inventory 10 times each year and the other only five times. The company with 10 inventory turns should experience better cash flow and more sales.

Thus, inventory turnover — and the related inventory turnover ratio — is a powerful key performance indicator.

Inventory Turnover Ratio

There are at least a couple of ways to calculate an inventory turnover ratio: (i) total sales divided by ending inventory or (ii) cost of goods sold divided by average inventory.

The calculations produce different results. The method you choose depends on which provides a better view of your company’s inventory and sales performance.

Sales and ending inventory. Many investors use a company’s sales and its ending inventory to calculate its inventory turnover ratio.

For example, for the fiscal year ended January 31, 2020, The Home Depot reported total revenue of $110.2 billion, a cost of revenue (roughly the cost of goods sold) of $72.7 billion, and an inventory balance of $14.5 billion (which I will use as a stand-in for both ending inventory and average inventory), according to Yahoo! Finance.

We can calculate inventory turnover for a single public company (such as The Home Depot) and estimate the average turnover for an entire industry.

Using this method we could calculate Home Depot’s inventory turnover ratio as 7.6. Home Depot turns over its inventory about 7.6 times each year.

If we wanted to know home many days it takes The Home Depot to turn its inventory once, we could divide the number of days in the year by the inventory turnover ratio we just calculated.

Using this method, we would estimate that The Home Depot turns its inventory about once every 48 days. This method is generally a little optimistic since it includes the company’s profit when it takes total sales as its numerator.

COGS and average inventory. A second method is to divide the cost of goods sold by the average inventory for the time frame in view. This typically provides a more accurate view of inventory turnover because it excludes any markup.

Let’s continue with The Home Depot example, using $14.5 billion in average inventory and approximately $72.7 billion for the cost of goods sold.

Notice this method produces a different inventory turnover ratio. In this case, we would estimate that The Home Depot turns its inventory about once every 73 days.

This calculation, which is called “Days’ Sales of Inventory” or “Days’ Inventory,” can estimate how long it takes to get a return on investment for inventory purchases.

Interpreting Inventory Turnover

Knowing your company’s inventory turnover ratio won’t necessarily help you understand how the business is performing. For that, you need context.

First, estimate the average inventory turnover ratio for your industry. If you sell building supplies, tools, and items for do-it-yourself projects, calculating inventory turnover for companies such as Home Depot and Lowe’s could provide context.

Also, you could find industry inventory turnover estimates online. A quick Google search, for example, shows that grocery stores typically have an inventory turnover of 40.

Next, benchmark your company’s inventory turnover. Review your financial data and calculate an inventory turnover ratio for each month, quarter, and year for at least the past couple of years. Armed with an industry average and your company’s benchmark, you could better gauge your inventory performance.

High inventory turnover. For example, a relatively high inventory turnover compared to the industry or your past performance is a good indicator of healthy sales and efficient purchasing. Your company is apparently making good inventory investments without overstocking.

But a high inventory turnover could also indicate too few purchases. Are you, for example, running out of stock?

Low inventory turnover. Conversely, if your company’s inventory turnover is low when compared to your industry or your own past performance, you likely have a sales or purchasing problem.

Low sales could mean that demand for your products is waning or that new competitors have entered the market.

A relatively low inventory turnover could also mean that you had dead inventory or that your business has been placing too many orders.

In short, monitoring inventory turnover can help ensure that things are going well with your business. As an added step, evaluate inventory turnover and inventory sell-through rates together.

The inventory turnover ratio is an efficiency ratio that shows how effectively inventory is managed by comparing cost of goods sold with average inventory for a period. This measures how many times average inventory is “turned” or sold during a period. In other words, it measures how many times a company sold its total average inventory dollar amount during the year. A company with $1,000 of average inventory and sales of $10,000 effectively sold its 10 times over.

This ratio is important because total turnover depends on two main components of performance. The first component is stock purchasing. If larger amounts of inventory are purchased during the year, the company will have to sell greater amounts of inventory to improve its turnover. If the company can’t sell these greater amounts of inventory, it will incur storage costs and other holding costs.

The second component is sales. Sales have to match inventory purchases otherwise the inventory will not turn effectively. That’s why the purchasing and sales departments must be in tune with each other.

Formula

The inventory turnover ratio is calculated by dividing the cost of goods sold for a period by the average inventory for that period.

Average inventory is used instead of ending inventory because many companies’ merchandise fluctuates greatly throughout the year. For instance, a company might purchase a large quantity of merchandise January 1 and sell that for the rest of the year. By December almost the entire inventory is sold and the ending balance does not accurately reflect the company’s actual inventory during the year. Average inventory is usually calculated by adding the beginning and ending inventory and dividing by two.

The cost of goods sold is reported on the income statement.

Analysis

Inventory turnover is a measure of how efficiently a company can control its merchandise, so it is important to have a high turn. This shows the company does not overspend by buying too much inventory and wastes resources by storing non-salable inventory. It also shows that the company can effectively sell the inventory it buys.

This measurement also shows investors how liquid a company’s inventory is. Think about it. Inventory is one of the biggest assets a retailer reports on its balance sheet. If this inventory can’t be sold, it is worthless to the company. This measurement shows how easily a company can turn its inventory into cash.

Creditors are particularly interested in this because inventory is often put up as collateral for loans. Banks want to know that this inventory will be easy to sell.

Inventory turns vary with industry. For instance, the apparel industry will have higher turns than the exotic car industry.

Example

Donny’s Furniture Company sells industrial furniture for office buildings. During the current year, Donny reported cost of goods sold on its income statement of $1,000,000. Donny’s beginning inventory was $3,000,000 and its ending inventory was $4,000,000. Donny’s turnover is calculated like this:

As you can see, Donny’s turnover is .29. This means that Donny only sold roughly a third of its inventory during the year. It also implies that it would take Donny approximately 3 years to sell his entire inventory or complete one turn. In other words, Danny does not have very good inventory control.